Complaints

Section 13(1)(c) of the Public Audit Act, 2004 (Act No. 25 of 2004) provides for a mechanism to objectively investigate and resolve complaints aimed at the manner in which the Auditor-General of South Africa (AGSA) performs its statutory audits.

In addition, paragraph 34 (c) of International Standards on Quality Management (ISQM) states that in designing and implementing responses in accordance with paragraph 26, the firm shall establish policies and procedures for receiving, investigating and resolving complaints and allegations about failures to perform work in accordance with professional standards and applicable legal and regulatory requirements, or non-compliance with firm’s policies and procedures established in terms of this ISQM.

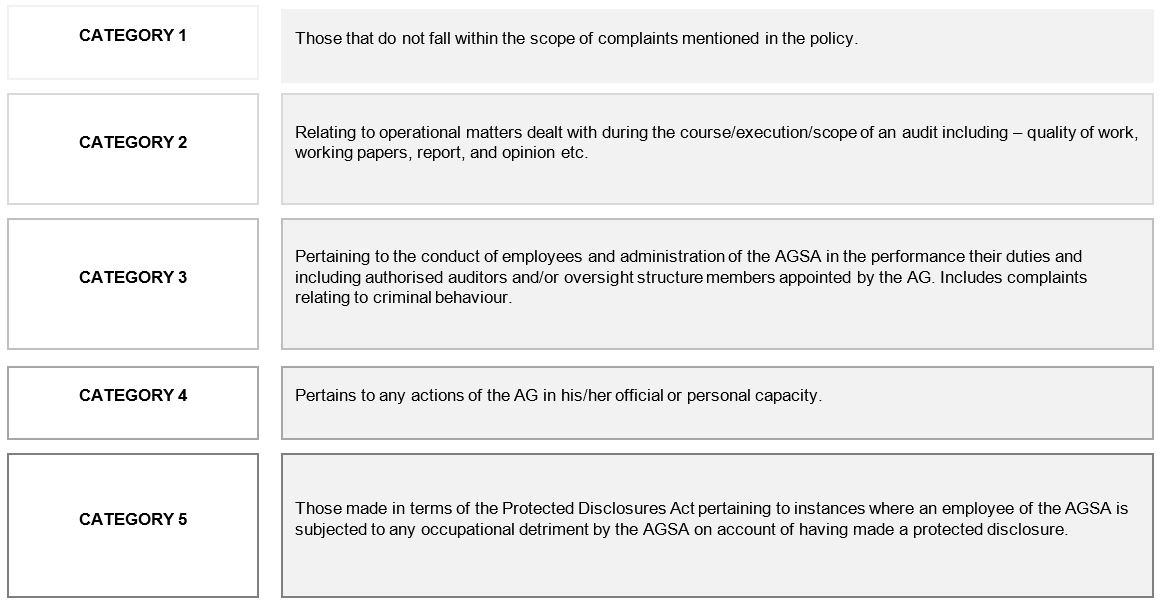

Based on the nature of the complaints, cases are classified into the following categories for investigation in line with the AGSA’s complaints policy:

All complaints, which are classified above according to the complaints policy may be referred to the AGSA by following the link that is provided on the website. Complaints other than those classified as category 2 complaints will be handled in terms of the AGSA’s complaints policy.

The AGSA’s Complaints policy can be accessed by clicking here.

Category 2 complaints (audit-related disputes) are handled in terms of the AGSA’s audit dispute resolution policy.

Audit disputes

When there are disagreements between auditors and auditees with respect to audit findings communicated to the auditee’s management during the audit such disagreements should preferably be resolved before the audit is finalised and the auditor’s report is signed.

All audit disagreements should be dealt with by raising them at the engagement team level with the engagement manager responsible for the audit. The engagement manager, with the support of the responsible deputy business unit leader and business unit leader will attempt to resolve the contested matter with the auditee.

If the audit disagreement relates to accounting standards and / or legislation, it is encouraged that the management of a provincial institution should refer the matter to the provincial accountant-general (PAG) and the management of a national institution should refer the matter to the appropriate unit of the Office of the Accountant-General (OAG) of the national treasury. The information provided by the PAG and/or OAG will be duly considered in an effort to find resolution on the audit disagreement.

Where the audit disagreement cannot be resolved between the engagement manager and the auditee, the matter becomes an audit dispute which must be formally escalated.

Audit disputes together with category 2 complaints will be handled in terms of the AGSA’s audit dispute resolution policy. The escalation of audit disputes and category 2 complaints will occur gradually in accordance with the mechanism provided for in the policy starting with the responsible head of portfolio, and thereafter if required, with the responsible head of audit.

The AGSA’s Audit dispute resolution policy can be accessed by clicking here.